- Milk Road Crypto

- Posts

- 🥛 Do this to 2x your $BTC 💀

🥛 Do this to 2x your $BTC 💀

...there’s just one catch ⚰️

GM. This is Milk Road, the newsletter that is skipping its weekly recap to nerd out on a new crypto tool we just discovered (that we didn’t know we needed)...

We have a pitch for you:

You give us 10 Bitcoin, and we give you 20 Bitcoin back.

…the only catch is, to claim your 20 $BTC – you must die.

We know, we know – that’s an obvious “no thank you” and maybe even a “where do you get off saying something like that to me on a lazy Sunday morning??”

But we’re willing to bet that by the end of this newsletter – you’re going to find yourself considering it (this is you 👇).

Let’s start with a moment of honesty…

When we got pitched this story, I didn’t want to do it.

Why? ‘Cause it was about Bitcoin life insurance.

(“Ah yes, life insurance – the cornerstone of an exciting Sunday read”)

But then I started to dig into the math…

And this mundane subject got real exciting, real fast!

(Hell, I’m even starting to play with the idea of taking coverage out for myself).

Here’s why:

It's idiot proof inheritance planning for your Bitcoin

You don't have to die to reap the benefits (you can take out tax-free loans against your policy)

If you don't utilize the loans, you’re guaranteed to pass more Bitcoin on to your family than you started with

(Brb, putting this on my vision board 👇)

Let’s start here…

1/ It’s idiot proof planning, disguised as life insurance.

Fun fact: The best investors are all dead.

Seriously.

Fidelity (one of the largest asset managers in the world) ran a study on their best-performing client accounts – and over a 10-year period, they found the highest returns came from ones where the account holder was dead.

The takeaway? Invest like a dead person.

(Buy → hold → don’t mess with it).

The same thing applies to Bitcoin – in the long-term, it’s better hodl’d.

‘Cause when an asset goes from $0.01 to $98k+ in fifteen or so years, you don’t need to trade it!

Which makes Bitcoin life insurance an ideal planning tool for long-term holders.

2/ The potential growth

Ok, so in preparation for this section, we peppered Meanwhile (the first and only life insurance company denominated in Bitcoin) with a whooole bunch of questions…

“How do payments work?”

“What are the payout ratios for each age bracket?”

“When my girlfriend asks me if I’d still love her if she were a worm, how should I respond?”

They answered some (though, unfortunately, not all) of those questions…

Payments are made in $BTC, and the payout ratios are based on your age and health.

But this alone was still enough to get our team chattering in Discord about all sorts of compound interest strategies, and where Bitcoin denominated life insurance could fit.

Cause once you map the projected returns of Bitcoin over the nex—

You know what?

How about I just show you with an example…

A healthy 30 year old gets somewhere in the range of a 1:2 ratio on their policy (for every 1 $BTC they pay, their policy pays out 2 $BTC).

And the policies are paid into by the customer over 10 years.

So let’s say (using round numbers for the sake of my sanity), you pay 1 $BTC a year for coverage, over a 10 year period…

Once that period is up – you don’t have to pay into the policy anymore. You’re done.

Any time after that, your family gets a tax-free payout of 20 $BTC, once you meet your maker.

Ok, but how much are they getting paid in dollar terms?

Let’s say I’m a healthy 30 year old (I’m neither, but let’s just pretend for a second here)...

Say I pay 1 $BTC per year for the next 10 years and lock in my policy pay out of 20 $BTC → spend the following 40 years enjoying my life → then curl my toes up at the age of 80…

That means 50 years have passed since I started my policy.

Over the last 10 years (2014-2024) $BTC has grown an average of 68.3% per year.

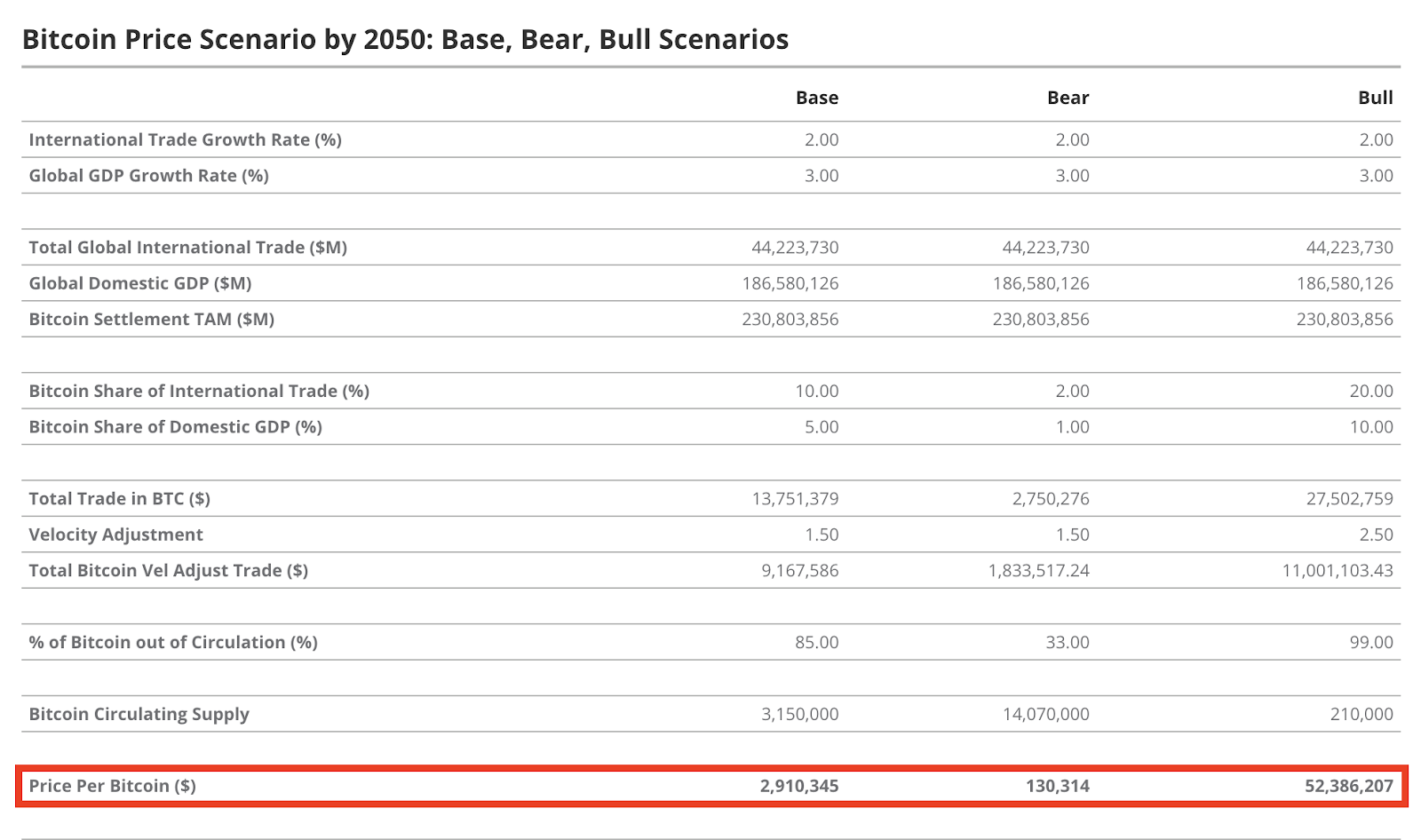

And between now and 2050, VanEck estimates it will grow like so:

Base case: roughly 14.4% per year (reaching $2.91M by 2050)

Bull case: roughly 27.8% per year (reaching $52.38M by 2050)

Let’s choose the weaker option and assume that $BTC only appreciates at 14.4% until 2050, and appreciates at 5% for every year after that…

Paying 1 $BTC per year, starting today with $BTC at $98k would mean the total cost of the policy would be ~$2.12M.

If I live to 80, the 20 $BTC my family would receive upon my death would be worth…wait for it…

$25,129,631.92.

Not too shabby! (And that’s just using VanEck’s base-case hypothesis).

In this case, I’d be seeing a policy return of roughly 5% per year over 50 years – which WAY outpaces the insurance industry’s average of 1-3.5%

And if you’re sitting there saying “Yeah, but I’d just invest that $BTC myself, selling into cycle peaks, and buying into cycle lows – that’d be way better for my family”

You’re not wrong! That’s an awesome plan.

…but:

Are you going to be able to stick to it? (Fidelity’s study begs to differ)

If you’re already paying for life insurance – why not make it a Bitcoin-backed policy?

Feel those mental wheels turning?

Good – ‘cause now it’s time for the main course…

3/ Taking tax-free loans against your policy

Now, we get it – by contributing to a Bitcoin-backed life insurance policy, you’re essentially locking up your $BTC forever (at least, from your perspective).

That can be a tough pill to swallow.

What if you want to use it to build out a new investment strategy? Or simply just spend some of it?

Simple: take out a tax-free policy loan.

Meanwhile allows you to take out a Bitcoin loan against your policy – and the borrowed Bitcoin gets a new cost basis, so you can sell it without incurring capital gains tax.

The real kicker? You never have to pay it back! (Instead, Meanwhile will deduct it from your final policy payout).

This way – if you find an opportunity that you just can’t pass up, you know the funds are there at your disposal.

Plus, if you want to be REALLY savvy with your taxes, you can buy a policy with 40% of your $BTC holdings, and keep it in your estate.

So if $BTC goes to the moon, your death benefit will scale with the $BTC in your estate (helping to cover estate taxes).

See…it’s happening…you’re considering it!

Told you that’d happen!

Ok, let’s land this plane! ‘Cause this is just about all the typing my fragile little fingers can handle right now…

If you want to learn more about $BTC-backed life insurance policies, there’s literally only one game in town (and by ‘town’ we mean ‘the world’).

Keen to learn more? Click below 👇

MILKY MEMES 🤣

RATE TODAY’S EDITION

What'd you think of today's edition? |

ROADIE REVIEW OF THE DAY 🥛

VITALIK PIC OF THE DAY

DISCLAIMER: None of this is financial advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions. Please be careful and do your own research.